Natural gas prices climbed to a nearly two-year high, driven by immediate weather-related demand and a bullish long-term outlook for global energy consumption.

In the short term, forecasts for below-average temperatures across the northern hemisphere—including North America, Europe, China, and Japan—are expected to significantly increase daily heating demand as these regions, which account for more than two-thirds of global gas consumption, enter their peak heating season. This has bolstered sentiment, with limited downside for prices likely until well into 2025.

Beyond the seasonal factors, the long-term outlook for natural gas remains robust. Rising electricity demand as the race for artificial intelligence accelerates, is projected to grow power consumption for such facilities by 10–15% annually through 2030, potentially accounting for up to 5% of global power demand by that time.

Natural gas is expected to play a pivotal role as a baseload energy source in this transition, given its current dominance in power generation. In the US, natural gas powers approximately 40–45% of electricity production, while globally, that share is closer to 25%. However, as more countries transition from coal to gas, the share of gas in electricity generation is anticipated to increase.

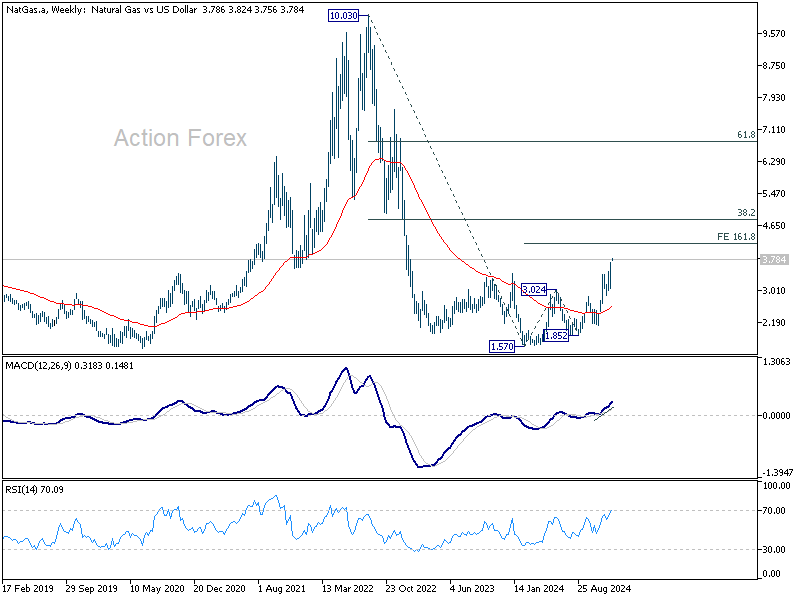

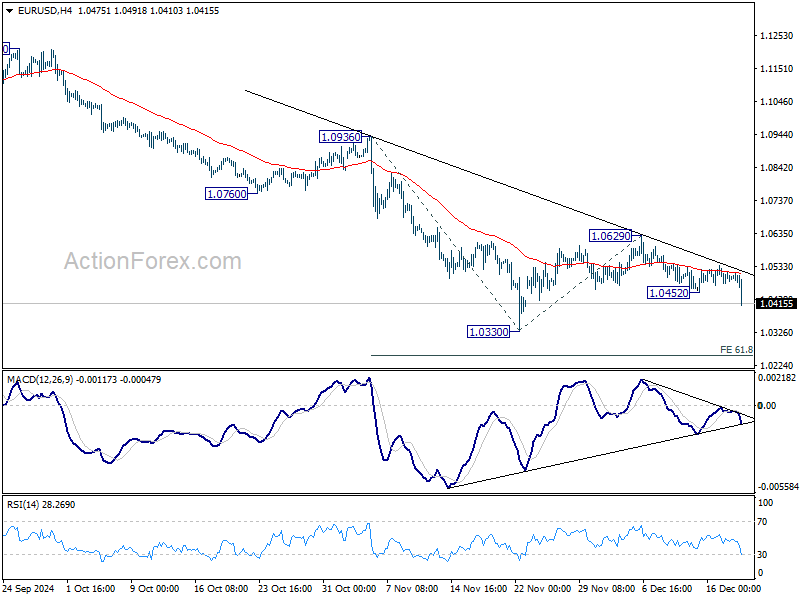

Technically, the break of 3.446 resistance last week was an important sign of underlying medium term momentum. Rise from 1.570 (Feb low) is now expected to continue to 161.8% projection of 1.570 to 3.024 from 1.852 at 4.204.

Nevertheless, momentum should target to wane above 4.204, and, in particular, as it approaches 38.2% retracement of 10.03 to 1.570 at 4.80.

US initial jobless claims falls -1k to 219k

US initial jobless claims fell -1k to 219k in the week ending December 21, slightly higher than expectation of 218k. Four-week moving average of initial claims rose 1k to 227k.

Continuing claims rose 46k to 1910k in the week ending December 14, highest since November 3, 2021. Four-week moving average of continuing claims rose 3k to 1881k.

Full US jobless claims release here.